Taiwan Semiconductor Manufacturing Company reported record-breaking second-quarter 2026 results on July 16, with revenue reaching US$40.2 billion and net profit surging 77.4% year-on-year to a fresh all-time high on relentless demand for AI accelerators from customers such as NVIDIA, Apple and AMD.

Revenue And Margins Blow Past Guidance

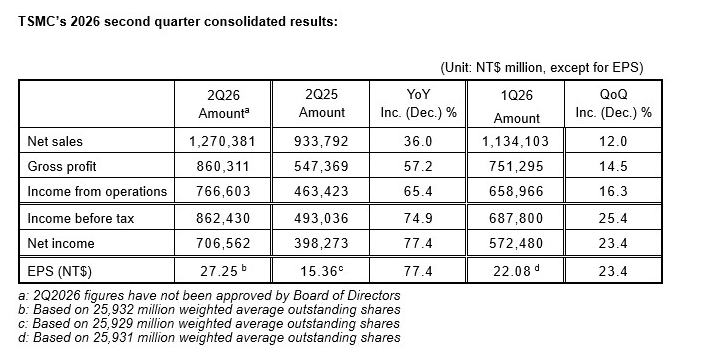

Revenue for the quarter came in at NT$1.27 trillion, up 36.0% year-on-year and 12.0% quarter-on-quarter, hitting the upper end of TSMC's previous US$39-40.2 billion guidance range. Net profit attributable to shareholders reached NT$706.56 billion (about US$22 billion), up 77.4% year-on-year and 23.4% quarter-on-quarter, well above the NT$632.6 billion consensus in the LSEG SmartEstimate. Diluted earnings per share of NT$27.25 (US$4.31 per ADR) rose 77.4%.

Profitability also topped internal guidance. Gross margin climbed to 67.7%, above TSMC's 65.5-67.5% range, with operating margin at 60.3% versus a 56.5-58.5% forecast. Management said higher capacity utilisation and cost improvements more than offset dilution from overseas fabs, and the quarter benefited from a NT$63.2 billion (US$1.97 billion) one-time gain from the sale and remeasurement of Vanguard International Semiconductor shares.

HPC Now Two-Thirds Of The Foundry

High-performance computing, TSMC's shorthand for AI accelerator, CPU and networking silicon, accounted for 66% of revenue, up 20% quarter-on-quarter and cementing the segment as the foundry's dominant growth engine. Smartphone revenue slid four points to 22%. Advanced nodes at 7nm and below now generate 77% of wafer revenue, with 3nm at 30%, 5nm at 33% and 2nm already contributing 3% as ramp-up begins.

What Wall Street Is Watching Next

The stock barely moved on the release, with investors saving their reaction for the analyst call and any lift to full-year revenue growth or capital expenditure targets. TSMC's June revenue already broke records on the way into today's print, and CoWoS advanced-packaging capacity is reportedly sold out through year-end. That is the same bottleneck cited in the Google TPU foundry battle and the Meta MTIA reallocation to Samsung. Continued AI capex from hyperscalers, combined with 2nm ramp discipline, will decide whether TSMC's gross margin can hold above the 65% floor into 2027, even as Arizona and Kumamoto fabs weigh on unit economics.

Reporting based on Q2 2026 earnings coverage from TradingKey, Reuters and Phemex analysis.